Content

- Summary

- Gem market

- Geographical structure of the world diamond market.

- Players in the global diamond market

- Russian diamond market

- Synthetic diamond market

- Regulation of the diamond market

- Consequences of the COVID-19 pandemic

Anton Tabakh, Managing Director for Macroeconomic Analysis and Forecasting, Expert RA

Anastasia Podrugina, lecturer at the Faculty of World Economy and International Politics, National Research University Higher School of Economics

The main tasks of the diamond exchange

Diamond exchanges (clubs) are the epicenter of the global trade in precious stones, the main participants of which are manufacturers, dealers and brokers. The largest diamond centers are located in Israel, Canada, USA, Belgium, South Africa, and India.

For the convenience of conducting trading operations, the organizers have developed a separate infrastructure. There are entire diamond hubs - special territories where the entire production cycle is concentrated.

The main tasks of the diamond exchange:

- Improving sales efficiency for diamond miners and diamond manufacturing companies.

- Creation of an optimal pricing tool and influence on price trends in the global market.

- Transferring part of the world rough and polished diamond market to your country.

- Providing our own jewelers with precious stones in the required volume.

- Independent research and certification of diamonds.

- Increasing the attractiveness of finished diamond products and individual stones for end consumers.

Summary

The situation on the diamond market in 2022 was called a “perfect storm” even before the start of the COVID-19 pandemic – in the spring of 2022, plans for a quick restoration of activity due to increased demand for diamonds and the subsequent sale of reserves were destroyed.

The pandemic has affected all elements of the global diamond market chains: upstream (diamond mining), midstream (diamond processing and jewelry manufacturing), downstream (distribution). Global value chains were disrupted due to restrictions on economic activity: production at some fields was suspended, cutters, due to market conditions, were forced to interrupt production during the quarantine, and demand for jewelry fell.

The recovery in the third quarter may be short-lived: the “second wave” of coronavirus and the corresponding restrictions on economic activity in the fourth quarter will most likely have a negative impact on the activities of all elements of the diamond chain.

Key points:

- Demand for final jewelry products decreased - sales in the second quarter fell to a record level, and a recovery was observed in the third quarter. The Asia-Pacific region (China, South Korea) played a major role in the recovery of demand. In addition, quarantine had a positive effect on the development of the jewelry sales channel via the Internet.

- The onset of a “second wave” of coronavirus and corresponding restrictions on economic activity in the fourth quarter of 2022 will likely have a negative impact on sales and financial performance in the second half of the year.

- The market structure of the diamond industry is an oligopoly: two main players are the Russian ALROSA and the British De Beers, which produce more than half of the diamonds. Moreover, 2019-2020 is likely to concentrate market power even more.

Additional theses:

- The leading countries in diamond production in 2022 remained unchanged: Russia, Botswana and Canada are the top three since 2017 (new mines opened in Canada in 2022). The main importers for 2022 are India (the world's cutting center), the EU (the largest diamond exchange in Belgium) and the UAE (a major diamond center).

- In 2022, the diamond market experienced a significant decline: a “perfect storm” was observed - several factors simultaneously had a negative impact on the market. There was a decrease in demand in the largest markets - China and the USA - due to geopolitical factors (trade war between the USA and China, protests in Hong Kong). In addition, the midstream diamond cutting segment, represented by 90% of Indian companies, came under pressure from a serious decline in bank financing.

- Diamond sales have declined significantly in 2022, and even as diamond production has been cut in response to lower sales, companies have accumulated significant inventories. The market expected deferred consumption in 2020 to offset losses incurred in 2022.

- The COVID-19 pandemic has negatively impacted all elements of the global diamond industry chain. Diamond mining in some fields was interrupted or even mothballed due to restrictions on economic activity. Large diamond miners, despite significantly reduced profits, are not experiencing serious financial problems. At the same time, “middle echelon” players experienced defaults in 2022, and perhaps the market recovery that began in the third and fourth quarters will not save some of them.

- Midstream in India, having not recovered from the problems of 2022, has imposed a nearly two-month moratorium on diamond imports. There are a large number of players in the facet of the diamond market value chain, and it is likely that not all of them will survive the market downturn in 2022, which could lead to consolidation of the sector and strengthening its bargaining position.

Gem market

Over the past decade, the natural stone market has grown largely due to increasing consumer demand in China. Another important consumer market for gemstones is North America.

Diamond is the most popular of all precious stones; in terms of sales volume, diamonds account for about 80% of the market. However, in 2022, the diamond market experienced some decline due to a decline in demand and some problems within the production chain.

The market for colored gemstones (ruby, sapphire, emerald) is small compared to the diamond market and is quite fragmented: there are many individual small players in the market, the products are not homogeneous, and therefore a full analysis of the market is difficult.

A significant portion of gemstones (about 85%) on the market today are synthetic, and further growth in this segment is expected due to lower prices for such stones.

Prices in the diamond industry

Diamond prices depend on the category of stone, which determines its quality:

- Technical - low quality diamonds that are used in industry;

- Jewelry - high quality, which is used in jewelry.

Diamond producers make the greatest profit from jewelry stones, since prices for industrial diamonds are an order of magnitude lower.

How is the price determined? The value of a stone depends on its “pedigree”, carat value, purity and color.

Geographical structure of the world diamond market.

Summary.

The leaders in diamond production are Russia, Botswana and Canada. The three leaders in diamond production for 2022 are Russia (33%), Botswana (17%), Canada (14%). In total, the three countries mine 63% of all diamonds in the world. In addition to the countries listed, development is underway in the Democratic Republic of the Congo, Australia, Angola, South Africa and some other countries. The total share of the listed countries in diamond production is 95%.

Largest diamond deposits

Russia – Mir, Aikhal, Udachny, Nyurbinsky, Botuobinsky (Western Yakutia), Lomonosov deposit, Grib deposit (Arkhangelsk region)

Botswana – Orapa, Letlhakane, Damtsha, Karowe (Central Botswana), Jwaneng (Southern Botswana)

Canada – Gacho Quay (Northwest Territories), Ekati, Diavik (Lake Gras), Renard (Quebec)

Angola – Catoca, Fucauma, Luarica

Australia – Argyll (Kimberley), Merlin (Northern Territory)

South Africa - Venice (Limpopo), Premier (Cullinan), Finsch (Northern Cape), Koffiefontein (Free State)

The geographical structure of production has not undergone significant changes over the past decade. Diamond production reached its highest level since 2004 (since the Kimberley Process began collecting production data) in 2022. The level of global production increased by 19.4% - from 126.4 to 150.9 million carats. Industry leaders - Russia and Botswana - increased production in 2022, but not very significantly (+5% and +12%, respectively), and the driver of growth was Canada, which increased diamond production by 78%. This is primarily due to the launch of the Gacho Quay and Renard mines, which allowed Canada to gain a foothold in third place in the list of largest diamond producers.

In 2022, global diamond production decreased by 7% - all leading countries except Russia reduced production (Botswana - (-3%), Canada - (-20%), Democratic Republic of the Congo (-14%), Australia - (- 8%)).

The dynamics of diamond production in value terms is influenced by prices: peaks in 2011 and 2014 are associated with rising diamond prices. In 2022, diamond production in value terms slowed down by 6% - affected by the fall in demand for diamonds in the US and China (the two largest markets) due to geopolitical and macroeconomic factors (the US trade war with China, protests in Hong Kong, slowdown in the world’s largest economies, increasing the overall level of uncertainty). In addition, the weakening of the yuan and rupee against the US dollar had a negative impact on demand in the diamond market.

High production volumes in 2022 and early 2022, coupled with weaker-than-predicted demand for diamonds, have led to falling prices and lower sales for major players in the diamond market. In addition, diamond mining companies have accumulated significant reserves of unsold stones, despite a decrease in production in physical terms in 2022. The accumulated diamonds were supposed to be sold with the market recovery in 2022.

The mined diamonds also differ in cost (which largely depends on the size). Among major producing countries, on average, the cheapest diamonds are found in the Democratic Republic of Congo and Australia, while the most expensive are found in Namibia and Lesotho.

Russia is a leader not only in diamond production, but also in proven reserves; as of 2022, proven reserves amount to 650 million carats - about 60% of the world's proven reserves.

The main importers of diamonds are India, the EU and the UAE. Their total share in diamond imports is 90%. The largest diamond exchanges are located in all three regions - in Mumbai, Antwerp (Belgium) and Dubai. India is the world's leading diamond cutter and producer; the country's share in diamond cutting is about 90%. Diamond production in India is insignificant, so India imports the bulk of its raw materials.

The decrease in total diamond imports in 2022 by 12% occurred both against the backdrop of a decrease in overall demand for diamonds (demand in the EU decreased by 12%, in China - by 33%), as well as against the backdrop of a 19% decrease in Indian imports due to internal reasons.

The decline in diamond imports in India began in 2022 due to problems with access to financing for Indian cutters following a scandal involving a major jewelry company's banking fraud. Indian diamond cutters, which rely heavily on external funding, have had a very negative impact. In addition, in 2022, the Indian Customs Service introduced increased requirements for the disclosure of information about imported diamonds: now, for the smooth import of rough diamonds, it is now required to disclose information about the country of origin of each stone, its size, shape, type, color, etc. The new requirements impose huge costs on cutters; the inventory of imported diamonds delays the process for weeks or even months.

Players in the global diamond market

Summary.

Alrosa and De Beers have accumulated reserves and reduced revenue. The rough diamond market is an oligopoly: in 2022, two market leaders - ALROSA and De Beers - produced more than half of all diamonds (69.3 million carats). There are other “middle echelon” players - Rio Tinto (the largest company in this category - 12% of the market), Petra Diamonds, Dominion Diamonds, AGD Diamonds, Lucara Diamond, Catoca.

The listed companies own mines in different countries:

- ALROSA – Russia (Yakutia), Angola

- De Beers – Botswana, Namibia, South Africa, Canada

- Rio Tinto - Australia, Canada

- Petra Diamonds – South Africa, Tanzania

The graph of diamond production dynamics by producer also shows a decline in production in 2022, associated with a decrease in aggregate demand. In the first quarter of 2022 (relative to the first quarter of 2022), all major diamond miners except Alrosa reduced production: Alrosa - +5%, De Beers - (-8%), Rio Tinto - (-18%), Petra Diamonds - ( -7%). The growth of Alrosa's diamond production is, in particular, associated with the discovery of the Verkhne-Munskoye deposit. Given the reduced demand, the increase in Alrosa's diamond production at the end of 2022 - 2020 led to an increase in the company's reserves.

Diamond production declined in the second quarter of 2022 as a result of restrictions on economic activity due to the COVID-19 pandemic. The most significant - at De Beers (-54%), virtually unchanged at Rio Tinto - in the second quarter, production fell by only 5.5%. The drop in Alrosa’s production was 42%, Petra Diamonds – 37%. However, already in the third quarter, production volumes began to recover, although they are still less than in the third quarter of 2022 (3Q2020 relative to 3Q2019: Alrosa - (-24%), De Beers - (-3.8%), Rio Tinto - ( -8%), Petra Diamonds – (-10%)).

Revenue in the first half of 2022 fell very significantly: Alrosa - (-46.4%), De Beers - (-53.8%), Rio Tinto2 - (-48%), Petra Diamonds - (-60.3%) (relative to the first half of 2022). The graph also shows the decline in revenue in 2022, which was mentioned above.

Due to a significant drop in revenue in 2022 and despite slightly reduced diamond production in 2022, diamond mining companies have accumulated quite significant reserves. Of the two largest diamond miners, only Alrosa publishes the volume of diamond reserves - the physical volume of reserves for the year (Q3 2022 - Q3 2020) increased by more than one and a half times - from 21.7 million carats to 30.6 million.

Of the four major diamond miners, two showed negative EBITDA in the first half of 2022 – Rio Tinto and Petra Diamonds. It should be noted that the mining concern Rio Tinto as a whole had positive EBITDA in the first half of 2022; only EBITDA for the diamond segment was negative.

Diamond mining is a high-margin industry; of the largest diamond miners, Alrosa also has the highest EBITDA margin. Even at the end of the first half of 2022, Alrosa showed high profitability - 42% against the background of near-zero profitability of other major players.

The volume of capital investments in the first half of 2022 also decreased: Alrosa - (-20%), De Beers - (-42.8%), Rio Tinto - (-13%), Petra Diamonds - (-76.8%) (vs. first half of 2019).

The diamond market in the global economy is characterized by “jumping” indicators. And they also play a significant role in its development. Even those who have their very first experience in diamond mining.

For example, “Pipe named after Mushroom”. Initially, it was supposed to be sold to the Russian oil company. However, today it is being developed independently.

The annual level of diamond production in 2016 was able to reach 170 million carats. However, in subsequent years, production will increase slightly. By 2022, it will increase by only another 5 million carats. The fact is that the reserves currently being mined are gradually being depleted. But there are not so many new major projects emerging.

In addition, experts say that even if a new diamond deposit is discovered in the near future, preparatory and geological exploration work will still take a lot of time. That is, by 2022 the overall picture will not change much.

Russian diamond market

Summary.

The price of a carat for export is falling, and for import it is growing. The main destination of Russian exports is Belgium (70%), one of the largest diamond exchanges in the world is located in Antwerp. In addition, Russia exports diamonds to the UAE, India, Hong Kong, Israel; in 2019, 99% of exported diamonds were sent to these countries (97.6% in value terms).

Russia also imports diamonds, mainly from Belgium (54%), other import destinations are the UAE, Hong Kong, Great Britain, and Israel. In total, Russia imports 99% of all diamond imports from these countries (93.4% in value terms).

On average, Russia exports cheaper diamonds and imports more expensive ones. In 2022, the average price of one exported carat was $89.4, and the average price of one imported carat was $284.1.

In the second quarter of 2022, both exports and imports of diamonds from Russia expectedly decreased significantly: exports fell by 86% in physical terms (-87% in value terms), imports fell by 98% in physical terms (-82% in value terms) . In the second quarter of 2022, Russia continued to import only the most expensive stones - the average price of an imported carat was $2,991.

Synthetic Diamond Market

Summary.

The shadow segment of the business spoils the reputation of the natural stone market. The market for synthetic diamonds - diamonds grown in laboratories - occupies a small share of the market as a whole, according to various estimates - 3-4%. The main producers in this market are China and India, the market is growing rapidly - in 2022 its growth amounted to 15-20%. The main consumer of synthetic stones is the USA.

It is difficult to imagine that synthetic diamonds will be able to completely displace natural stones from the market. “Diamonds are forever,” De Beers declared in its 1940s advertising campaign. Although the market for artificial diamonds has its buyers, the so-called “Generation Z” is shifting towards a model of reasonable consumption that involves environmental and social responsibility.

However, the biggest threat to the natural stone market comes not from a change in consumption patterns, but from the shadow market. Currently, the market for synthetic diamonds has not fully developed into a separate market; synthetic diamonds are often mixed with natural diamonds: one can only be distinguished from the other in a gemological laboratory. According to Alrosa estimates, about 80% of laboratory-grown diamonds are sold according to this scheme. The semi-legal position of the market for artificial diamonds causes serious damage to the market for natural stones - a real “market for lemons” of Akerlof is being formed.

The market for lemons is a market model with information asymmetry published by J. Akerlof in 1970. Akerlof cited the example of the used car market, where buyers do not have reliable information about the quality of the car and are therefore not willing to pay a high price for a car that may be of poor quality. This leads to the displacement of high-quality cars from the market, and then to the complete disappearance of the market.

Diamond mining giants use various strategies to reduce information asymmetry. So Alrosa released a serial device, ALROSA Diamon Detector, which allows you to distinguish natural stone from laboratory-grown stone.

De Beers is investing in the production of synthetic stones; in 2018, the company created a separate brand, Lightbox, under which it sells products made from laboratory-grown diamonds.

One of the largest retailers of diamond jewelry, Tiffany & Co, states that it is not engaged and does not plan to sell jewelry with artificial diamonds. As one method of protecting against counterfeit natural diamonds and conflict stones, the company primarily purchases and sells individually registered diamonds larger than 0.18 carats (over 75% of its volume).

Diamond trends

The advent of synthetic stones marked the beginning of a new era in the history of diamonds. They are cheaper than natural ones (20-40%), while their characteristics are not inferior to their natural counterparts.

The profit from synthetic diamonds is almost 2 times higher than from natural diamonds. Therefore, according to forecasts, their production will increase in the near future.

Another important trend is the change of generations, which has influenced the nature of consumer preferences. Young people (19+) mainly pay attention to new technologies and brand positioning. They are critical by nature and less attached to things.

Regulation of the diamond market

Summary.

Russia will lead the process of protection against “blood” diamonds for another year. The diamond market - from mining to sales - is regulated quite carefully, although there are regulatory gaps.

The main direction of regulation of the diamond market is protection from so-called “blood diamonds”, stones, the proceeds from the sale of which are used to finance military operations of rebel groups in African countries (Angola, Sierra Leone, Liberia, Cote d'Ivoire and others).

At the international level, regulation is carried out through the Kimberley Process. The Kimberley Process is an international diamond certification scheme created in 2003 to combat illegal diamond mining and the financing of rebel groups from mined diamonds. Currently, 56 countries are participating in the Kimberley Process, collectively producing 99.8% of diamonds. Kimberley Process participants agree to comply with a set of requirements regarding the control of diamonds produced and the exchange of statistical data within the Kimberley Process, and to trade only with Kimberley Process countries that meet a minimum set of requirements. In 2022, Russia chaired the Kimberley Process, but due to the coronavirus pandemic, its chairmanship was also postponed to 2022, and Botswana’s turn to 2022.

The activities of the Kimberley Process are sometimes criticized for insufficient control over the implementation of requirements - it was not possible to completely eradicate the trade in “blood diamonds” in some African countries.

A significant part of the sale of legal diamonds is carried out through diamond exchanges (Belgium, India, Israel, Great Britain and others). The World Federation of Diamond Bourses, in particular, helps to unify trade practices.

Another area of regulation is the labeling of synthetic diamonds. The Kimberley Process is also developing labeling practices for all synthetic stones produced within participating countries. Such practices will help reduce information asymmetries and protect the natural diamond market.

Russia is also developing a system for marking precious stones: the Ministry of Finance estimated the volume of shadow turnover in Russia in the jewelry industry at 58%. From 2022, it is planned to launch a state integrated information system for precious metals and precious stones, which involves marking all precious stones, including rough and polished diamonds, and precious metals. Despite the importance of such labeling described above, it should be noted that it imposes some costs on all participants in the production chain, but the additional costs are likely to be most significant for retailers: before July 1, 2021, all stock will be required to be labeled.

Largest exchanges in the world

Five exchanges rule the roost in the global diamond trade. They present the best examples of stones of any type, color, size, cut. People from all over the world come to do business, but getting to the world's largest exchanges is not so easy.

Top 5 largest diamond exchanges in the world:

- Ramat Gan

- Antwerp

- London

- Toronto

- Mumbai

Ramat Gan

Here is the main diamond exchange of Israel, which is a huge complex of organizations operating in the diamond market. More than 6,000 people visit the exchange every day.

The active development of the exchange was facilitated by the friendly policy of the country's leadership. Rough diamonds are imported and exported duty-free, preferential lending conditions are offered to manufacturers, and their interests are lobbied at the international level. At the same time, the activities of all enterprises, including jewelry stores and consulting agencies, are strictly controlled.

Having its own stone cutting factories also gives the country a competitive advantage in the market.

The Diamond Exchange in Ramat Gan reliably maintains its leadership position despite the emergence of other similar organizations. It's all about maintaining access to consumer markets in the US, Hong Kong and other Far Eastern countries. In conditions of intensified competition, Israel will occupy a dominant position for a long time.

Antwerp

Belgium has been considered the world's diamond trading center for over 500 years. In Antwerp, one and a half thousand wholesale and retail companies annually sell about 60% of all precious stones. The Antwerp Diamond Exchange (AWDC) employs more than two thousand participants, and the cutting of local cutting plants is recognized as one of the highest quality in the world.

Getting into the building of the Diamond Exchange itself is not so easy. The buyer will need an official invitation from a person who has the right to represent the interests of clients when concluding a transaction on its territory. Most of the crystals are sold wholesale to jewelry houses and businesses. However, a private person can also buy a diamond based on a recommendation.

London

The London Diamond Bourse (LDB) was founded after the end of World War II by refugees from Belgium. The first president of the exchange is Max Lack. Its services are available only to those who strictly adhere to the established code of conduct and hold a high position in the diamond industry. The total number of participants never exceeded more than 700 people.

In 2015, the London Exchange held its first open day.

Toronto

The Canadian exchange is one of the youngest. The first auction took place in January 2010. Since then, both bidders and experts have noted its great potential, which has allowed it to gain membership in the World Federation of Diamond Bourses.

The emergence of a new large platform for trading rough and polished diamonds is not accidental - Canada is the third largest producer of these precious stones, which were previously distributed through historically established sales channels. Having our own independent association is a chance for the Canadian diamond business to reach a new, more modern level.

Mumbai

It is impossible to imagine the jewelry world without Indian diamonds. Every year, India exports up to $20 billion worth of raw and cut precious stones (16% of all goods)! The organization of the Bharat Diamond Exchange was a natural continuation of the development of the Indian diamond business.

The country's authorities spent almost two decades creating the exchange, and in October 2010 it opened its doors. Dealers, appraisers, traders, representatives of diamond companies, banking and customs offices were located on hundreds of thousands of square meters in eight buildings of nine floors each.

The Diamond Exchange fully met expectations for an increase in the volume of supplies of Indian stones to international markets - already in 2011 its turnover amounted to more than $22 billion.

Consequences of the COVID-19 pandemic

Upstream

Summary.

Quarantined mines: not all will survive The two largest diamond miners - Alrosa and De Beers - decided to reduce production to prevent the formation of low-liquid residues. In addition, by the fall of 2022, both companies still reduced prices (Alrosa reported an average reduction of 10%) despite the fact that Alrosa previously followed a “price above volume” strategy, and De Beers followed a similar policy.

Both companies adjusted the trading session schedule, making the time frame softer. De Beers completely canceled the third cycle of diamond sales, and during the 4th and 5th cycles it allowed customers to refuse to purchase diamonds, which had an extremely negative impact on sales volumes. However, by the 8th cycle, sales volume had recovered to the level of the end of 2022.

Alrosa similarly invited customers to cancel the purchase in April-August 2022. Sales volumes during the crisis period remained at an extremely low level, but by October 2022 they also recovered.

In addition, in 2022, the world's largest diamond mine, Argyle (Australia), owned by Rio Tinto, whose production volume was about 14 million carats per year (about 10% of all diamond production), was scheduled to close. Combined with the decline in diamond production in response to the pandemic, there is likely to be a significant reduction in the supply of diamonds in the coming years.

Many diamond miners were unable to maintain their operating model during the pandemic and found themselves in serious financial difficulties. Large players (Alrosa, De Beers, Rio Tinto) do not have such financial problems, in particular due to the size of the company. In the second quarter of 2022, Alrosa increased its debt by almost one and a half times compared to the same period in 2022: in May it placed ruble bonds worth 25 billion rubles for a period of 5 years, in June – Eurobonds worth $500 million for 7 years, in addition , bank loans were attracted for 2 years to provide liquidity to operating activities. De Beers does not disclose data on debt obligations, but the parent company Anglo-American also increased the amount of debt, including one aimed at raising working capital for De Beers.

Among the “second-tier” players, a wave of bankruptcies has already begun in the diamond industry with the default of Dominion Diamond on April 24, 2022, and may continue with other bankruptcies. Dominion Diamond, in turn, filed a claim for protection from creditors, and is currently exploring options for debt restructuring and seeking new financing. In addition, the company soon plans to resume production at the Ekati mine, which was suspended in the spring of 2022 due to epidemiological restrictions.

Table 1. Credit ratings of major diamond mining companies. Source: compiled by the author.

| Fitch | Moody's | S&P | |

| ALROSA | BBB- (stable) 06/11/2020 | Baa2 (stable) 06/15/2020 | BBB- (stable) 06/09/2020 |

| De Beers (Anglo American) | BBB (stable) 05/05/2020 | Baa2 (negative) 11/24/2020 | BBB (stable) 05/12/2020 |

| RioTinto | A (stable) 05/05/2020 | A2 (stable) 10/01/2020 | A (stable) 02/13/2018 |

| Petra diamonds | Caa3 05/12/2020 | D (11.05.2020) | |

| Mountain Province Diamonds | CCC (negative) 08/27/2020 | Caa3 (negative) 07/20/2020 | CCC- (negative) 05/04/2020 |

| Dominion Diamond | D 04/24/2020 |

Source: compiled by the author.

Midstream

Summary.

India's diamond cutters are consolidating. The pandemic and subsequent restrictions on economic activity have caused serious damage to India, the largest diamond cutter. In the Indian cutting market there are thousands of small companies and hundreds of thousands of cutters who are unable to pay wages due to restrictions on economic activity. To support the industry and create the possibility of selling existing reserves, India announced a moratorium on diamond imports for two months (with a break). By September 2020, India's diamond imports had already recovered to $1,347.3 million, up 16% from September 2022.

Apparently, the pandemic did not harm the demand for large and expensive stones too much, but from medium stones the demand shifted towards cheaper analogues. Thus, exports of natural diamonds from India in April-September 2022 fell by 36.5% compared to the same period in 2022, while exports of synthetic diamonds increased by 14.6% over the same period. Imports of synthetic diamonds into India also increased by 36%, while demand for other precious stones and metals fell significantly. To some extent, this is due to the import ban, but the above-described factor of shifting demand was probably also influenced.

However, the recovery depends on the risk of a “second wave” of coronavirus in India: new restrictions on economic activity will undoubtedly negatively affect the activities of cutters.

As a result of the events described above, consolidation of the diamond cutting market in India is possible due to the exit of ineffective companies from the market. The emergence of multiple leaders can ease the funding problem through greater transparency and disclosure. In addition, in the event of oligopolization of the polished sector, changes in the global diamond production chain may occur: one or more major players with a serious bargaining position may emerge.

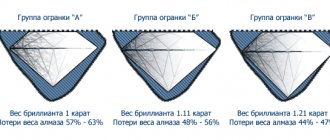

Diamond grading: GIA system

In 1953, the Gemological Institute of America (GIA) developed one of the most accurate diamond grading systems. Most gemological laboratories in the world still rely on the GIA “4C” classification to determine the value of stones.

The system classifies diamonds into five grades of quality: poor, fair, good, very good and excellent. The quality of diamonds is determined by 4 key parameters: carat weight, color, clarity and cut.

Weight

The weight of the mined gemstone directly affects its value. The weight and size of diamonds are measured in carats: 1 carat (ct) is equivalent to 0.2 grams.

Depending on their weight, diamonds are divided into small (up to 0.29 carats), medium (0.3-0.69 carats) and large (over 0.7 carats).

Typically, large minerals have a higher value, but some small stones are more valuable - if they have unique quality characteristics.

Color

Completely colorless “white” stones are the most expensive, as they are extremely rare in nature. The explanation for this is simple: the more transparent the diamond, the more it sparkles and shines.

Colored diamonds are graded using different criteria. Especially for “colorful” finds, GIA has developed a scale on which gemologists around the world determine the saturation of a particular shade.

Colored diamonds can have a wide variety of color inclusions. The most common shades are yellowish and white. The least common stones are red, blue, green and purple.

There are also diamonds of the so-called fancy shade. These include stones that are not included in the GIA scale. They are separated “by determining the hue, saturation, tones from light to dark and the uniformity of color distribution of the diamond.

Purity

Cleanliness is the degree to which chips, cracks, air bubbles and other defects are present both outside and inside the stone. It is noteworthy that stones without internal defects are valued more than diamonds that are “clean” on the outside.

The rarest diamonds are those without any internal inclusions or with minor defects that are not detected by the GIA standard grading method using a 10x magnification loupe.