"Protracted deficiency state"

The market is facing a shortage of rough diamonds. Global producers have exhausted their accumulated reserves, new deposits are not appearing, and demand is growing after the pandemic, said Sergei Takhiev, head of Alrosa’s corporate finance department. “Demand is huge and will likely remain strong. But supply has decreased, and our consumers understand that the market is moving into a very protracted state of shortage,” Takhiev said during a webcast organized by BCS Global Markets.

In the early 2010s, the market was balanced: the supply of diamonds of 128 million carats corresponded to demand, and jewelry products worth $65-$75 billion were sold annually. In 2016-2018, the supply increased to 151 million carats. But starting from 2019-2020, the market went down due to the retirement of old fields and the lack of commissioning of new ones, the top manager explained.

Advertising on Forbes

Material on the topic

“Now supply is about 25% lower than it was before coronavirus, and about 10% lower than at the beginning of 2010,” says Takhiev. The demand for diamonds, which fell due to the pandemic in 2020, has recovered, but the supply cannot keep up with it, agrees Alexey Kalachev, an analyst at Finam Group of Companies. Mining companies sold all the reserves that they had accumulated in 2019-2020 to cutting companies. At the same time, sales volume was greater than annual production. Alrosa sold off its reserves accumulated in 2019-2020 by the end of the second quarter of this year and since then has been selling off the top of everything it produces, Takhiev said.

Prices are going up

Diamond prices have already increased by 25% since the beginning of the year, including in the third quarter, diamond prices increased by 10%, reaching the 2022 level. The price increase is confirmed by senior investment analyst Andrey Lobazov.

According to Takhiev, average nominal prices for rough diamonds could rise to $180-200 per carat compared to the current $130 (in 2022 the price was $109 per carat). “But given the fact that there is a deficit, there is every chance to break even higher,” says Takhiev. Market supply will remain relatively stable at 110-120 million carats per year in the next 10 years, he believes.

Material on the topic

“The diamond industry has truly entered a state of structural scarcity, with many mines depleted or still closed due to the pandemic, while demand is booming. In such conditions, the rise in diamond prices, which will continue in 2022, will allow the market to return to a state of balance,” Veles Capital analyst Vasily Danilov told Forbes.

How does the diamond market work and what place does ALROSA occupy in it?

The famous marketing slogan of one of the largest diamond miners is no longer so relevant. No, people continue to associate diamonds with symbols of eternal love or wealth, but the world’s reserves of precious stones are gradually being depleted. If the trend continues, in a few years there may not be enough natural diamonds for everyone. Let's look at what the industry is like and what place the Russian diamond mining company ALROSA occupies in it.

Industry structure

Diamond production is divided into 3 main stages: upstream (mining), midstream (processing and manufacturing of jewelry), downstream (retail).

Upstream

Upstream or rough diamond mining is geographically concentrated in the countries of South Africa, Russia, Australia and Canada.

The cost of entering the diamond mining market is quite high, and therefore there are not many players in the industry. About 70% of all gemstones mined today are produced by the five largest companies.

De Beers (part of the Anglo American group) is a diamond mining company that previously occupied about 80% of the market. This company stood at the origins of the diamond industry, and it was with the light hand of De Beers marketers that the tradition of giving diamond rings arose. The company's monopoly position in the industry at the beginning of the 20th century was supplanted by miners from the USSR, Australia and Canada by the end of the century. Today, De Beers controls less than 1/3 of the market, ranking second in the world in terms of production volumes with 35.3 million carats of diamonds as of 2022. De Beers develops deposits in Botswana, South Africa, Canada and Namibia.

Rio Tinto is a publicly traded diversified mining company involved in the exploration, production and processing of natural resources. Rio Tinto's diamond business includes the Argyle (100% owned, Australia) and Diavik (60% owned, Canada) mines. In 2022, Rio Tinto produced 18.4 million carats of diamonds.

Petra Diamonds is a public diamond mining company that develops diamond deposits in South Africa and Tanzania. In 2017, Petra Diamonds produced 3.8 million carats of diamonds.

Dominion Diamond is a diamond mining company operating as part of The Washington Companies group of private companies. Dominion Diamond owns a 40% interest in the Diavik diamond mine (Canada) and an 89% interest in the Ekati diamond mine (Canada). The company's diamond production in 2022 at the Diavik deposit amounted to 3.0 million carats.

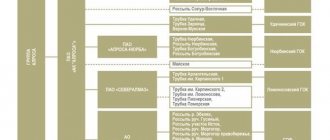

Russian diamond reserves are developed by ALROSA , which at the end of 2022 produced 36.7 million carats - the first result in the world. ALROSA's operational activities are concentrated in two regions of the Russian Federation: the Republic of Sakha (Yakutia) and the Arkhangelsk region. The largest deposits (pipes) of the company: Mir, Yubileinaya, Udachnaya. In addition, ALROSA participates in the capital of the diamond company Catoca Ltd in Angola (32.8% share) and plans to develop mining in Zimbabwe.

ALROSA's diamond reserves are the largest in the world and amount to 1,030 million carats, according to JORC data for 2016. Mining costs are at minimal levels: $44 per carat, with an average selling price of $160 per carat. This ensures EBITDA margins on par with the industry's top performers.

Diamond mining is the highest-margin stage; it is at this stage that a significant part of the cost of precious stones is formed. EBITDA margin for ALROSA is 57% for the third quarter of 2022, De Beers announces a 58% margin in the upstream segment at the end of 2016, Petra Diamonds - 39% for the first half of 2018.

At the end of 2022, ALROSA reduced production volumes by 7% to 36.7 million carats from 39.6 million carats in 2022, in particular, due to the accident at the Mir mine. The company plans to produce 38 million carats in 2022 by increasing production at the Udachnaya mine to 5.7 million carats and launching the Verkhne-Munskoye deposit (1.8 million carats).

Starting from 2022, ALROSA changed its dividend policy, switching to semi-annual payments and establishing free cash flow (FCF) as the dividend base instead of net profit.

The minimum limit for dividends is 50% of net profit under IFRS, but an additional portion of FCF is paid depending on the ratio of net debt to EBITDA. The company's new policy is more attractive to investors due to an increase in dividend yield, frequency and stability of payments. The company's FCF has been consistently increasing in recent years and over the last 4 quarters (through Q3 2022) almost reached RUB 100 billion, and the net debt to EBITDA ratio as of September 30, 2022 is at 0.2x. In this case, investors have reason to expect 70% of FCF as dividends.

For the first half of 2022, 5.93 rubles were paid. per share, which corresponded to a 5.9% dividend yield. For comparison: for the whole of 2017, 5.24 rubles were paid. per share. Based on the results of the second half of 2018, you can expect approximately 5.4 rubles. per share, which corresponds to a yield of around 5.4% at current quotes.

Midstream

Midstream includes diamond cutting and jewelry making. At this level, there is a clear leader - India, which accounts for more than 90% of global imports of rough diamonds and 75% of exports of processed stones. The country retains its leading position due to cheap labor and the relative ease of attracting financing.

Midstream is characterized by low margins - on average 1-3% and significant competition. There are about 5 thousand companies operating in the segment, according to Bain & Company.

In recent years, this segment has undergone significant changes. Decrease in the profitability of cutters to record lows (0% and below) in 2014-2015. provoked the exit of the least efficient participants from the market, and a process of consolidation began in the industry, which is still ongoing.

An important feature of midstream is seasonality - cutters traditionally increase their reserves of raw materials at the beginning of each year. At the same time, the seasonal demand for diamonds is stronger, the higher the sales of diamond jewelry during the Christmas holidays and Chinese New Year.

Downstream

Downstream - sales and retail. The key sales market for rough and polished diamond products is the USA. As of 2022, the US market share is 48%.

The relationship between US GDP and demand for diamond jewelry is quite clearly visible.

The Chinese market is promising for the diamond industry with a share of 16% and good prospects for growth in the well-being of the country's citizens. Between 2009 and 2015, diamond jewelry sales in the country grew at an average rate of 12%. In 2016, the dynamics turned out to be negative -4.8%, but already in 2022, demand began to increase again (+0.9%). It is expected that in the future the penetration of diamonds into the Chinese market will continue at an accelerated pace.

India also plays a significant role in the consumption of diamond products, however, in 2022, an increase in interest rates from 6% to 6.5% and accelerating inflation in the country provoked a reduction in consumer demand. There are no signs of a change in the situation against the backdrop of tightening monetary policies by world central banks in the near future.

Industry prices

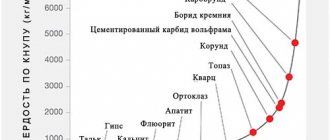

Diamond prices vary significantly depending on the quality of the stone. There are two large categories:

1) industrial diamonds are minerals of lower quality, used for industrial purposes;

2) jewelry diamonds are high-quality raw materials used to create jewelry.

Although industrial diamonds occupy a significant share of mined stones (about 30%), their cost is several times lower than high-quality analogues.

Diamond mining companies generate most of their profits from jewelry stones. In particular, ALROSA's share of industrial diamonds accounts for 2% to 4% of its revenue.

Jewelry diamonds are a marginal commodity, but non-standard, and there is no single pricing method. The value of a stone depends on factors such as carat, color, and purity. The “pedigree” of the stone plays an important role—diamonds mined through “bloody” means are not in great demand. The centers of diamond trading can be considered auctions in Antwerp, Mumbai, Bombay, Dubai and London.

One of the tools you can use to track diamond prices is the Diamond Index from the International Diamond Exchange. The index is calculated based on prices from the world's largest diamond auctions.

Diamond trends

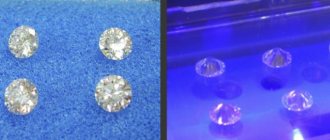

A notable trend in the diamond industry is the entry of synthetic (artificially grown) stones into the jewelry market. Such diamonds are grown in laboratories, and their characteristics are not inferior to their natural counterparts.

The use of synthetic diamonds in industrial production reaches 97%, but now they are beginning to enter the jewelry market. Prices for artificial stones are 20-40% more attractive compared to those mined in the ground, but the growth of demand for them is hampered by the position of the largest players in the market. Mining companies lobby for the uniqueness of natural minerals, maintaining higher prices for natural diamonds. According to estimates by ALROSA Supervisory Board member Alexey Moiseev, the volume of the market for synthetic stones after cutting in 2022 is 20%, and this share is constantly increasing.

The existing premium for the “naturalness” and purity of the history of the stone has become a driver for the active introduction of new technologies into the industry. In particular, from 2017-2018. Thanks to projects based on blockchain technology, buyers can track the entire production chain and verify the natural origin of the purchased stone. Artificial intelligence and real-time control systems have found their application in reducing the ever-increasing costs of diamond mining.

Another important trend is generational change. De Beers notes in its study that the consumer profile is changing. The older generation (40+ years old) is being replaced by millennials (21-39 years old) and generation “Z” (0-20 years old). For young people, new technologies and social responsibility of companies play a big role in consumption. They are critical in their judgments, and the need for love and family is as high as that of older people.

The change of generations is reflected in consumer preferences: the growing influence of the brand on the cost of stones is becoming one of the features of the diamond market. By 2022, the share of branded diamonds could reach 30%, predicts the international consulting company McKinsey.

Forecasts and prospects

Consulting company Bain & Company believes that global demand for rough diamonds will grow at an average annual rate of approximately 1% to 2% until 2030, with supply dynamics ranging from -1% to +1% per year.

The key markets for diamond products are expected to be the USA, China and India. In the USA, a steady increase in real income of the population by 1.5-2.5% per year will stimulate demand for jewelry products. The development of the Chinese economy and the emergence of a broad middle class will become the driver of a sustainable long-term trend for the growth of diamond consumption in this country. India is now one of the major consumers of diamond jewelry. It is predicted that market growth will continue until 2030 due to the development of the middle class and increasing demand for wedding jewelry.

ALROSA expects a drop in global supply in the diamond market by 2022. This is due to the gradual depletion of easily accessible reserves through the depletion of mines. This is stated in her presentation.

The international consulting company McKinsey shares a similar opinion. Diamond production will remain at approximately the same levels until 2025, after which a gradual decline will begin against the backdrop of mine output and rising capital and operating costs, according to the company’s research.

Baseline forecasts suggest that diamond inventories will gradually decline with demand growing moderately. An increasing shortage can support prices for precious stones, which is positive for the margins of diamond mining companies. ALROSA, which has one of the largest diamond reserves in the world, could be the main beneficiary of such a scenario.

BCS Broker